Check out the companion video to this article:

https://www.youtube.com/watch?v=cBwigNigYtU

Is Adobe (ADBE) a Buy?

Based on a stock selection guide analysis, Adobe looks like a buy opportunity with a projected annualized return of 19.9%. Adobe’s recent acquisition of Figma caused Adobe’s stock price to fall off of a cliff last year but has since partially recovered going into 2023. With a strong cash position and low debt, Adobe looks to be in a strong position to continue their investments in the content creation niche.

So, Adobe recovered somewhat from a major drop in late summer 2022. Their analyst meeting from October wasn’t great news but had a minimum amount of bad news. The market has shown a little more confidence since then.

What is Adobe?

Adobe is a software company focused on content creation. Back in the day they focused on actual print media but has since then transformed into serving web media to multimedia. The company started back in 1982 with a language called PostScript which allowed what was the 1980s and 1990s buzzword of wysiwyg (what you see is what you get) and help start a whole graphic user interface revolution that is ancient history now.

Then the company created Adobe Photoshop, which is still a cornerstone application for them and how a lot of people get introduced to the Adobe world. So just like people get introduced to the Microsoft world through Microsoft Office tools like Word and Excel, Adobe - which has its own sort of design language and specific way you have to get used to driving it - a lot of their customers comes through Photoshop including myself. They then move on to other Adobe tools. Then they developed what is likely their most familiar product the PDF. Even if you don't know the name Adobe Acrobat, the PDF document format is Adobe’s free intro to the world. In fact, they currently estimate that the number of PDF documents in existence are somewhere in the trillions. Think about how that is on a per capita basis for everyone in the world. But this gives them exposure to just about any kind of document or content creation in the world.

Then moving on, macromedia was a competing product Suite that they acquired and integrated into their products. Omniture was a significant acquisition that has created the other leg of Adobe – the experience cloud. The next company with the little white infinity symbol is the Creative Cloud. This company spurred their migration from selling new software to selling annual licenses which has really driven the company's growth in the last decade.

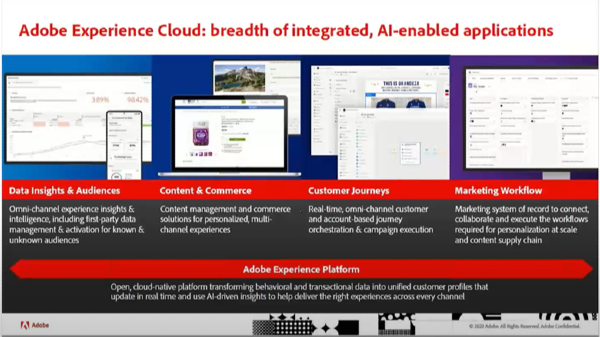

Adobe’s Experience Cloud

So, we talked about the Creative Cloud, so here is the experience cloud. This came from that one key acquisition of Omniture.

Adobe is involved in online advertising, but not to provide ads or sell ads to you, but to help you manage your ad content and campaigns. The first product on the left provides customers with insight and data about their advertising and omni-channels. The software provides insights across platforms and allows customers to compare platform X to platform Y, so you know you’re getting your bang for your buck.

But they've grown (as you know see with their products to the right) into helping you actually execute on that insight. Most advertisers need to decide which platforms to advertise on. Do we advertise on Meta Platforms or on Google? Which of those platforms are we getting value from? Adobe’s platform manages the whole experience to discover what platforms are working together and do your advertising tools have a role in effective advertising and getting consumers to buy our products. We can understand this even if that isn't the point where they click.

So, this product has become a very sophisticated Suite. It's not quite 20% of Adobe’s revenue but it's the fastest growing segment right now. The Adobe Experience Cloud works behind the scenes and integrates very well with the creation and management of content.

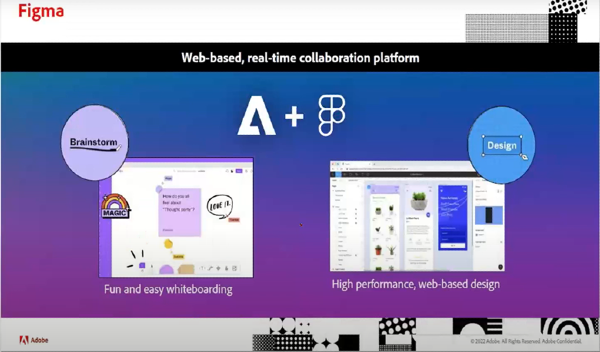

Adobe’s Acquisition of Figma

So, let’s discuss what's been Adobe’s most recent adventure last quarter. So, the trouble started with the announcement of the acquisition of Figma, which is a very small company. Figma had $200 million in revenue in 2021 and Adobe announced they would purchase Figma for $20 billion. That's the kind of buyout you can only find in the technology sector.

Read More: Adobe Defends its $20 Billion Deal for Figma

The initial reaction from pundits and analysts was, “In what world does this acquisition make sense?”

So, Figma has two primary applications. It is an online collaborative design tool. One is a whiteboard space – think of an open sandbox. You probably have used Figma or similar whiteboards in other tools like GoToMeeting. The other one is a much more sophisticated product design tool. What Adobe found was that a significant amount of their customers overlapped with Figma’s customer base even though Figma is a much smaller company. Note, Figma also gives away their entry level tools like Adobe, so a lot of adobe customers were also using these Figma tools.

Another article talks about this acquisition of this very tiny company as a move to control the entire creative market that some were labeling as a monopolist move.

I had a wise person, that was involved in labor relations tell me that when you make a good decision in a difficult circumstance, the way you know it was a good decision is not when everyone is at peace with your decision, but instead that you're getting an equal amount of complaining from both sides.

So, either this was a colossally stupid move where Adobe is just burning billions of dollars either to snuff out a potential competitor who has a small customer base or it's a very shrewd move to keep a near monopoly in the creative world.

In the price graph in the lower left corner, you can see through the summer of 2022, Adobe’s price has drifted with the rest of the tech market until it fell off a cliff in early September. This cliff is easy to identify due to the high volumes and rapid price fallout.

This cliff was the market’s reaction to the acquisition as market participants screamed, “Why in the world would you pay $20 Billion to this company?”

But then some more opinions have come out that were more favorable towards the deal, but as of Q4 2022 Adobe still sat significantly below its six-month averages.

Figma's two tools are Fig Jam and Figma. The simpler tool is called Fig Jam and then their Figma tool – their namesake tool - on the right is a much more robust full product design software.

So, Adobe doesn't really talk about the future of either of these two tools. Adobe is talking about overall goals of product design, collaborating on the web, and the future of creativity. I can only guess Adobe has been coy about what they're using Figma for. I think that there is some back-end intellectual property that Figma has that Adobe found either Superior to their own or complementary to what they have and that's what's really providing the value.

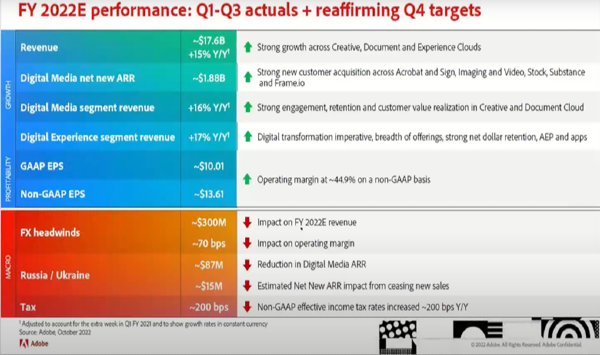

Adobe’s Recent Earnings Results

So, these are the key points. The news wasn't so bad in the last analyst call and you can see for 2022 they have affirmed their targets. On the bottom you can see the headwinds that they're claiming including FX (Forex exchange). Adobe does significant business outside of the US that is not denominated in US dollars, so they are impacted by forex like so many companies. Unfortunately, the war in Ukraine has also affected their financial outlooks.

For next year their latest guidance is slightly below their prior guidance. Their prior guidance for 2023 in total revenue was $19.85 billion and their revised guidance is $19.1 to $19.3 Billion. So, it ends up that revenue has a 9% year-over-year growth for the overall company. You can see from the second line how important the digital media segment is. The growth in this dominant segment is moving the company’s revenue growth. Even though digital experience on the third line is growing 13%, its growth hasn't really moved the total company needle yet. But in time the digital experience segment will be significant as it keeps growing faster than the overall company.

Then finally on the bottom, GAAP earnings per share are in line with revenue growth so we always want to look make sure sales and profit are up, straight, and parallel.

Read More: Why do sales and profit need to be up, straight, and parallel on a stock selection guide?

What is Adobe’s (ADBE) Forecast?

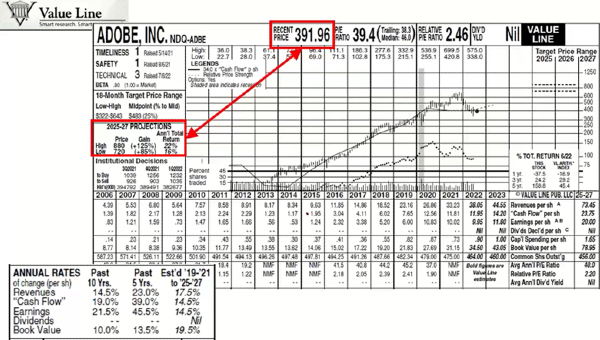

So, let’s take a look at our trusted advisors at value line. This value line is from early August so it's before that precipitous fall in September. That was when Adobe was at a price of $391 and it's at $323 as of Q4. This sheet still had a low expected return of 16% and a high of 22%. Again, looking in the lower left at the annual rates of growth, revenue reached 17.5% and earnings were at 14.5%. This was more robust than the latest guidance given for next year by Adobe, but in line with the constant currency numbers that Adobe gave.

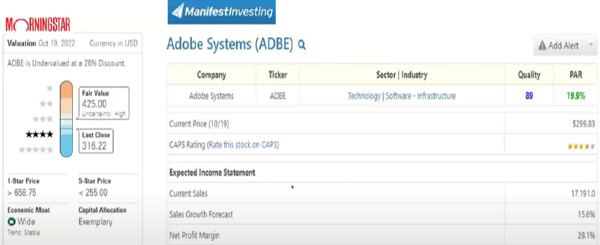

From our other advisors at Morningstar, they gave Adobe a four-star rating on here. It's five-star price is at $255. Adobe’s price fell within the $270 range after the acquisition announcement, so Adobe’s price never actually reached this five-star price.

Adobe’s Stock Forecast thru 2023 to 2026

So, pessimistically, you could imagine what the price might really go down to.

From Manifest Investing, we have a 19.9% projected annual return (PAR), high quality, and sales growth in the teens which aligns with other resources.

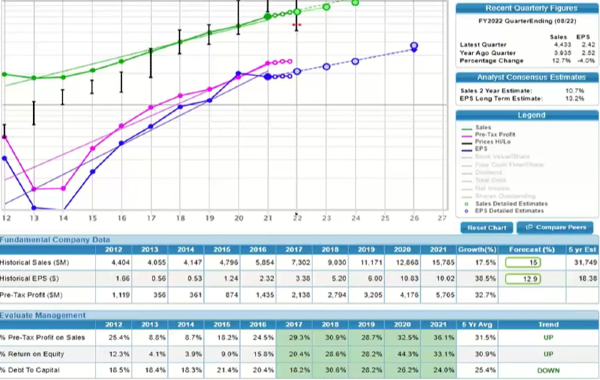

So, looking at the SSG, on the left of the chart from 2012 to 2015, there was a dip in profit due to a change over from selling perpetual licensing software to annual licensing software.

I actually owned Adobe before and sold it somewhere in 2013 because I was skeptical of that growth. In retrospect, that was a poor decision on my part. I did fine with my alternative stock choices, but I've always been looking for a place to get back into Adobe since then.

Looking back at 2022 we are near the 52-week low in Q4. That's a good opportunity, and in fact you have to look back to 2020 to find a price in that range.

I have turned on the analyst estimates. I've put in the value line estimated earnings per share for our 2026 forecast and you can see how my numbers line up with their estimates. For historical sales, I chose a nice round 15% growth. For EPS, since it is growing a little bit slower than sales, I'll keep my forecast conservative.

Adobe paid cash plus shares for Figma. And while Adobe does have a robust share buyback plan like many tech companies in lieu of a dividend, I have modeled here that they are going to maintain their share count and not reduce it in the next five years. In effect, they would recover from the dilution from buying Figma in five years. I think that estimate is pretty conservative. The company has not given specific targets but has certainly said that they're going to focus on share buybacks with the extra cash they have.

Pre-tax profit, and return on equity looks excellent. Looking at debt to Capital they've kept this metric under control by keeping debt low. They have a significant stock buyback plan and they have made significant acquisitions before Figma, yet they have kept their debt manageable and have used their excellent profitability to take care of these large cash intensive projects.

Adobe does have a P/E ratio that trends in a range that is typical for tech stocks. You need to be comfortable with a high P/E ratio if you're going to own this company. The average high P/E is above 50 and around 30 for an average low. To be conservative, I've calculated the high price range using the average low P/E ratio of 30 instead of the high P/E ratio of 50. This models the extreme situation where the markets continue to be pessimistic about tech stocks for the next five years as much as they are today. For the low price, I used the 2020 low price of $255.

Read More: How to Interpret the Price to Earnings Ratio

These estimates seem reasonable for a company that is a solid owner of its particular market niche and has grown its last major acquisition into an entirely different division of a company which now commands about 20% of their revenue.

Check out the companion video to this article:

https://www.youtube.com/watch?v=cBwigNigYtU

I/we have a position in an asset mentioned

Check out the companion video to this article: https://www.youtube.com/watch?v=cBwigNigYtU

Is Adobe (ADBE) a Buy?

Based on a stock selection guide analysis, Adobe looks like a buy opportunity with a projected annualized return of 19.9%. Adobe’s recent acquisition of Figma caused Adobe’s stock price to fall off of a cliff last year but has since partially recovered going into 2023. With a strong cash position and low debt, Adobe looks to be in a strong position to continue their investments in the content creation niche. So, Adobe recovered somewhat from a major drop in late summer 2022. Their analyst meeting from October wasn’t great news but had a minimum amount of bad news. The market has shown a little more confidence since then.

Source: Adobe Financial Analyst Meeting 2022 Presentation

What is Adobe?

Adobe is a software company focused on content creation. Back in the day they focused on actual print media but has since then transformed into serving web media to multimedia. The company started back in 1982 with a language called PostScript which allowed what was the 1980s and 1990s buzzword of wysiwyg (what you see is what you get) and help start a whole graphic user interface revolution that is ancient history now.

Then the company created Adobe Photoshop, which is still a cornerstone application for them and how a lot of people get introduced to the Adobe world. So just like people get introduced to the Microsoft world through Microsoft Office tools like Word and Excel, Adobe - which has its own sort of design language and specific way you have to get used to driving it - a lot of their customers comes through Photoshop including myself. They then move on to other Adobe tools. Then they developed what is likely their most familiar product the PDF. Even if you don't know the name Adobe Acrobat, the PDF document format is Adobe’s free intro to the world. In fact, they currently estimate that the number of PDF documents in existence are somewhere in the trillions. Think about how that is on a per capita basis for everyone in the world. But this gives them exposure to just about any kind of document or content creation in the world.

Then moving on, macromedia was a competing product Suite that they acquired and integrated into their products. Omniture was a significant acquisition that has created the other leg of Adobe – the experience cloud. The next company with the little white infinity symbol is the Creative Cloud. This company spurred their migration from selling new software to selling annual licenses which has really driven the company's growth in the last decade.

Adobe’s Experience Cloud

Source: Adobe Financial Analyst Meeting 2022 Presentation

So, we talked about the Creative Cloud, so here is the experience cloud. This came from that one key acquisition of Omniture.

Adobe is involved in online advertising, but not to provide ads or sell ads to you, but to help you manage your ad content and campaigns. The first product on the left provides customers with insight and data about their advertising and omni-channels. The software provides insights across platforms and allows customers to compare platform X to platform Y, so you know you’re getting your bang for your buck.

But they've grown (as you know see with their products to the right) into helping you actually execute on that insight. Most advertisers need to decide which platforms to advertise on. Do we advertise on Meta Platforms or on Google? Which of those platforms are we getting value from? Adobe’s platform manages the whole experience to discover what platforms are working together and do your advertising tools have a role in effective advertising and getting consumers to buy our products. We can understand this even if that isn't the point where they click.

So, this product has become a very sophisticated Suite. It's not quite 20% of Adobe’s revenue but it's the fastest growing segment right now. The Adobe Experience Cloud works behind the scenes and integrates very well with the creation and management of content.

Adobe’s Acquisition of Figma

Source: Adobe Financial Analyst Meeting 2022 Presentation

So, let’s discuss what's been Adobe’s most recent adventure last quarter. So, the trouble started with the announcement of the acquisition of Figma, which is a very small company. Figma had $200 million in revenue in 2021 and Adobe announced they would purchase Figma for $20 billion. That's the kind of buyout you can only find in the technology sector.

The initial reaction from pundits and analysts was, “In what world does this acquisition make sense?” So, Figma has two primary applications. It is an online collaborative design tool. One is a whiteboard space – think of an open sandbox. You probably have used Figma or similar whiteboards in other tools like GoToMeeting. The other one is a much more sophisticated product design tool. What Adobe found was that a significant amount of their customers overlapped with Figma’s customer base even though Figma is a much smaller company. Note, Figma also gives away their entry level tools like Adobe, so a lot of adobe customers were also using these Figma tools.

Another article talks about this acquisition of this very tiny company as a move to control the entire creative market that some were labeling as a monopolist move.

I had a wise person, that was involved in labor relations tell me that when you make a good decision in a difficult circumstance, the way you know it was a good decision is not when everyone is at peace with your decision, but instead that you're getting an equal amount of complaining from both sides. So, either this was a colossally stupid move where Adobe is just burning billions of dollars either to snuff out a potential competitor who has a small customer base or it's a very shrewd move to keep a near monopoly in the creative world.

In the price graph in the lower left corner, you can see through the summer of 2022, Adobe’s price has drifted with the rest of the tech market until it fell off a cliff in early September. This cliff is easy to identify due to the high volumes and rapid price fallout. This cliff was the market’s reaction to the acquisition as market participants screamed, “Why in the world would you pay $20 Billion to this company?” But then some more opinions have come out that were more favorable towards the deal, but as of Q4 2022 Adobe still sat significantly below its six-month averages.

Source: Adobe Financial Analyst Meeting 2022 Presentation

Figma's two tools are Fig Jam and Figma. The simpler tool is called Fig Jam and then their Figma tool – their namesake tool - on the right is a much more robust full product design software.

Source: Adobe Financial Analyst Meeting 2022 Presentation

So, Adobe doesn't really talk about the future of either of these two tools. Adobe is talking about overall goals of product design, collaborating on the web, and the future of creativity. I can only guess Adobe has been coy about what they're using Figma for. I think that there is some back-end intellectual property that Figma has that Adobe found either Superior to their own or complementary to what they have and that's what's really providing the value.

Adobe’s Recent Earnings Results

Source: Adobe Financial Analyst Meeting 2022 Presentation

So, these are the key points. The news wasn't so bad in the last analyst call and you can see for 2022 they have affirmed their targets. On the bottom you can see the headwinds that they're claiming including FX (Forex exchange). Adobe does significant business outside of the US that is not denominated in US dollars, so they are impacted by forex like so many companies. Unfortunately, the war in Ukraine has also affected their financial outlooks.

Source: Adobe Financial Analyst Meeting 2022 Presentation

For next year their latest guidance is slightly below their prior guidance. Their prior guidance for 2023 in total revenue was $19.85 billion and their revised guidance is $19.1 to $19.3 Billion. So, it ends up that revenue has a 9% year-over-year growth for the overall company. You can see from the second line how important the digital media segment is. The growth in this dominant segment is moving the company’s revenue growth. Even though digital experience on the third line is growing 13%, its growth hasn't really moved the total company needle yet. But in time the digital experience segment will be significant as it keeps growing faster than the overall company.

Then finally on the bottom, GAAP earnings per share are in line with revenue growth so we always want to look make sure sales and profit are up, straight, and parallel.

What is Adobe’s (ADBE) Forecast?

So, let’s take a look at our trusted advisors at value line. This value line is from early August so it's before that precipitous fall in September. That was when Adobe was at a price of $391 and it's at $323 as of Q4. This sheet still had a low expected return of 16% and a high of 22%. Again, looking in the lower left at the annual rates of growth, revenue reached 17.5% and earnings were at 14.5%. This was more robust than the latest guidance given for next year by Adobe, but in line with the constant currency numbers that Adobe gave.

From our other advisors at Morningstar, they gave Adobe a four-star rating on here. It's five-star price is at $255. Adobe’s price fell within the $270 range after the acquisition announcement, so Adobe’s price never actually reached this five-star price.

Adobe’s Stock Forecast thru 2023 to 2026

So, pessimistically, you could imagine what the price might really go down to. From Manifest Investing, we have a 19.9% projected annual return (PAR), high quality, and sales growth in the teens which aligns with other resources.

So, looking at the SSG, on the left of the chart from 2012 to 2015, there was a dip in profit due to a change over from selling perpetual licensing software to annual licensing software.

I actually owned Adobe before and sold it somewhere in 2013 because I was skeptical of that growth. In retrospect, that was a poor decision on my part. I did fine with my alternative stock choices, but I've always been looking for a place to get back into Adobe since then.

Looking back at 2022 we are near the 52-week low in Q4. That's a good opportunity, and in fact you have to look back to 2020 to find a price in that range.

I have turned on the analyst estimates. I've put in the value line estimated earnings per share for our 2026 forecast and you can see how my numbers line up with their estimates. For historical sales, I chose a nice round 15% growth. For EPS, since it is growing a little bit slower than sales, I'll keep my forecast conservative. Adobe paid cash plus shares for Figma. And while Adobe does have a robust share buyback plan like many tech companies in lieu of a dividend, I have modeled here that they are going to maintain their share count and not reduce it in the next five years. In effect, they would recover from the dilution from buying Figma in five years. I think that estimate is pretty conservative. The company has not given specific targets but has certainly said that they're going to focus on share buybacks with the extra cash they have.

Pre-tax profit, and return on equity looks excellent. Looking at debt to Capital they've kept this metric under control by keeping debt low. They have a significant stock buyback plan and they have made significant acquisitions before Figma, yet they have kept their debt manageable and have used their excellent profitability to take care of these large cash intensive projects.

Adobe does have a P/E ratio that trends in a range that is typical for tech stocks. You need to be comfortable with a high P/E ratio if you're going to own this company. The average high P/E is above 50 and around 30 for an average low. To be conservative, I've calculated the high price range using the average low P/E ratio of 30 instead of the high P/E ratio of 50. This models the extreme situation where the markets continue to be pessimistic about tech stocks for the next five years as much as they are today. For the low price, I used the 2020 low price of $255.

These estimates seem reasonable for a company that is a solid owner of its particular market niche and has grown its last major acquisition into an entirely different division of a company which now commands about 20% of their revenue.

Check out the companion video to this article:

https://www.youtube.com/watch?v=cBwigNigYtU

I/we have a position in an asset mentioned