A credit score indicates a person's creditworthiness or how apt they are to pay off a loan. It is a calculation based on your credit reports. FICO scores are used by 90 percent of top lenders. FICO stands for Fair Isaac Co.

The standard gives lenders, employers, or landlords an idea of how a consumer handles money. Bill Fair and Earl Isaac were an engineer and a mathematician who founded the Fair Isaac Corporation in 1956.

The organization built the original credit scoring system two years later, in 1958. The three major credit bureaus – Experian, TransUnion, and Equifax - were using the system by 1991 to help banks with lending decisions.

FICOs are not the only credit scores. Because they are so widely used, knowing your FICO score helps you understand how lenders evaluate the risk when applying for credit or a loan. Other credit scores use different formulas than FICO and may not be an accurate representation of the scores a lender uses to assess your credit profile.

What Factors Affect FICO Scores?

A wide range of information is used to calculate a FICO score. Income is not a factor, nor are race, marital status, zip code, gender, employment history, education, or age. Any information that does not predict future credit performance or is not found on a credit report is not used.

The data on credit reports are used to calculate FICO scores. There are five main categories used from a report. The list and relative importance is

- Payment history – 35%

- Amounts owed – 30%

- Length of credit history – 15%

- Credit mix – 10%

- New credit – 10%

FICO scores are unique. The importance of the categories listed above can differ. Scores for those who have not used credit very long are calculated differently than those with a longer credit history. As the information on a credit report changes, so does the assessment of the factors used to determine FICO scores.

Because FICO scores evolve frequently, it is impossible to measure the factors' precise impact on the FICO score without analyzing the entire credit report. The levels of importance may differ for the general population from other profiles.

Good FICO Scores

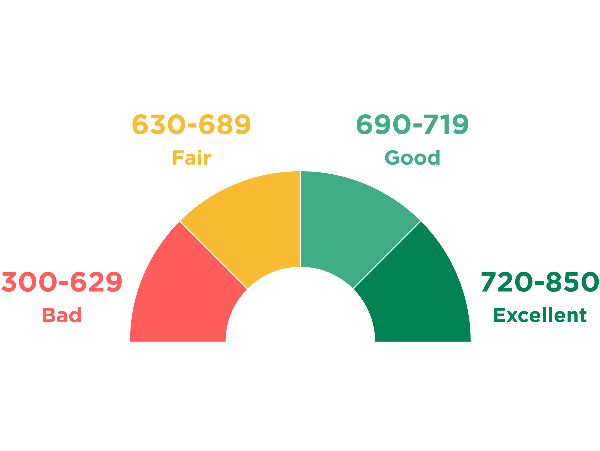

The range of FICO scores is typically from 300 to 850. Industry-specific scores range from 250 to 900. The higher the score is, the lower the credit risk. What is 'good' depends on the lender. One lender may offer lower interest rates to those with a FICO score above 730, while another only lends to those with a FICO score above 760. A breakdown of FICO score ranges as a general guide is as follows.

- Less than 580 – Poor

- 580-669 – Fair

- 670 to 739 – Good

- 740 to 799 – Very Good

- 800 and above – Exceptional

A 'Poor' score indicates the person is a risky borrower. Some lenders grant credit to those with a 'Fair' score. Most lenders approve credit for those with a 'Good' score. A 'Very Good' score indicates a person is a very dependable borrower. 'Exceptional' is a score well above the U.S. consumer average.

How to Attain a High FICO Score

Research shows people who have higher FICO scores tend to

- Make monthly payments on time

- Have low credit card balances

- Only apply for credit when needed

- Have a long credit history

When a person applies for a mortgage, auto loan, or credit card, lenders want to know the risk they would take by loaning money. Lenders order credit reports and request a credit score based on the reports' information. The credit score helps lenders assess a credit report. Your credit report is a snapshot of the credit risk at a particular time.

The first thing lenders look for is whether past credit accounts were paid on time. It helps determine the amount of risk they will take. Payment history is the FICO score factor of most importance. Owing money and having credit cards does not automatically flag you as a high-risk borrower that earns a lower FICO score.

The amount of your available credit used is what matters. If balances are close to the limits, a lender may see that as an indication you are overextended and deem you a higher risk for default. Long credit history is a positive for FICO scores but is not a requirement.

FICO scores consider how long credit accounts have been in existence, such as the age of the newest account, the age of the oldest account, and the average age of all accounts. How long since certain accounts have been used is also a factor.

The mix of mortgage loans, finance company accounts, installment loans, retail accounts, and credit cards is also considered in FICO scores. It is unnecessary to have all of these. Opening multiple accounts within a short period represents a greater risk of creditworthiness, especially if the person does not have a long credit history.

RECAP

Lenders want to ensure they will be repaid. They want to know if a borrower paid past debts on time. Other questions are how much debt they already have and who else has been approached for a loan. FICO scores help lenders answer these questions through a mathematical formula that makes faster, safer, and fairer lending decisions. It is essential to understand how credit behaviors and activities are considered in calculating FICO scores. When applying for credit, it is very likely the lender will use FICO scores to make an approval decision.

A credit score indicates a person's creditworthiness or how apt they are to pay off a loan. It is a calculation based on your credit reports. FICO scores are used by 90 percent of top lenders. FICO stands for Fair Isaac Co.

The standard gives lenders, employers, or landlords an idea of how a consumer handles money. Bill Fair and Earl Isaac were an engineer and a mathematician who founded the Fair Isaac Corporation in 1956.

The organization built the original credit scoring system two years later, in 1958. The three major credit bureaus – Experian, TransUnion, and Equifax - were using the system by 1991 to help banks with lending decisions.

FICOs are not the only credit scores. Because they are so widely used, knowing your FICO score helps you understand how lenders evaluate the risk when applying for credit or a loan. Other credit scores use different formulas than FICO and may not be an accurate representation of the scores a lender uses to assess your credit profile.

What Factors Affect FICO Scores?

A wide range of information is used to calculate a FICO score. Income is not a factor, nor are race, marital status, zip code, gender, employment history, education, or age. Any information that does not predict future credit performance or is not found on a credit report is not used.

The data on credit reports are used to calculate FICO scores. There are five main categories used from a report. The list and relative importance is

FICO scores are unique. The importance of the categories listed above can differ. Scores for those who have not used credit very long are calculated differently than those with a longer credit history. As the information on a credit report changes, so does the assessment of the factors used to determine FICO scores.

Because FICO scores evolve frequently, it is impossible to measure the factors' precise impact on the FICO score without analyzing the entire credit report. The levels of importance may differ for the general population from other profiles.

Good FICO Scores

The range of FICO scores is typically from 300 to 850. Industry-specific scores range from 250 to 900. The higher the score is, the lower the credit risk. What is 'good' depends on the lender. One lender may offer lower interest rates to those with a FICO score above 730, while another only lends to those with a FICO score above 760. A breakdown of FICO score ranges as a general guide is as follows.

A 'Poor' score indicates the person is a risky borrower. Some lenders grant credit to those with a 'Fair' score. Most lenders approve credit for those with a 'Good' score. A 'Very Good' score indicates a person is a very dependable borrower. 'Exceptional' is a score well above the U.S. consumer average.

How to Attain a High FICO Score

Research shows people who have higher FICO scores tend to

When a person applies for a mortgage, auto loan, or credit card, lenders want to know the risk they would take by loaning money. Lenders order credit reports and request a credit score based on the reports' information. The credit score helps lenders assess a credit report. Your credit report is a snapshot of the credit risk at a particular time.

The first thing lenders look for is whether past credit accounts were paid on time. It helps determine the amount of risk they will take. Payment history is the FICO score factor of most importance. Owing money and having credit cards does not automatically flag you as a high-risk borrower that earns a lower FICO score.

The amount of your available credit used is what matters. If balances are close to the limits, a lender may see that as an indication you are overextended and deem you a higher risk for default. Long credit history is a positive for FICO scores but is not a requirement.

FICO scores consider how long credit accounts have been in existence, such as the age of the newest account, the age of the oldest account, and the average age of all accounts. How long since certain accounts have been used is also a factor.

The mix of mortgage loans, finance company accounts, installment loans, retail accounts, and credit cards is also considered in FICO scores. It is unnecessary to have all of these. Opening multiple accounts within a short period represents a greater risk of creditworthiness, especially if the person does not have a long credit history.

RECAP

Lenders want to ensure they will be repaid. They want to know if a borrower paid past debts on time. Other questions are how much debt they already have and who else has been approached for a loan. FICO scores help lenders answer these questions through a mathematical formula that makes faster, safer, and fairer lending decisions. It is essential to understand how credit behaviors and activities are considered in calculating FICO scores. When applying for credit, it is very likely the lender will use FICO scores to make an approval decision.