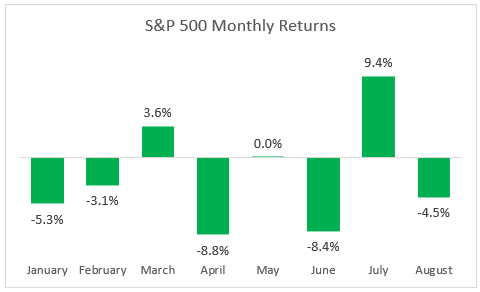

Monthly returns tell the story

A quick glance at the chart below tells the story. The rally-sellers dominated the action in January, February, April, June, and August. The dip-buyers tried to take back control in March, May, and July. They nearly succeeded in the two months from June 16 to August 16 by taking the market up 17.4%. It has all been downhill since then.

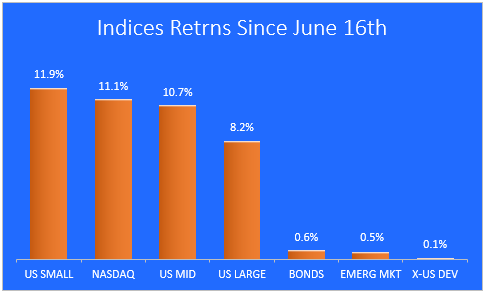

Global Market Indices

Today's market X-ray shows the returns for each index, asset class, sector, and so on, since the recent low point on June 16th. You can see what's leading the market and what's lagging behind. For reference, the S&P 500 is up 7.9% since June 16th..

Of the global indices, US small caps are in the lead, followed by the NASDAQ.

On a relative basis, U.S. stocks are trouncing non-US stocks and global bonds since June 16th.

All of the return data in this article is from Morningstar.

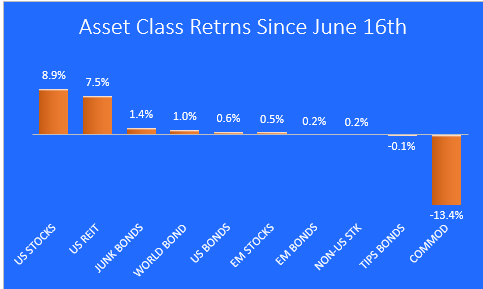

Global Asset Classes

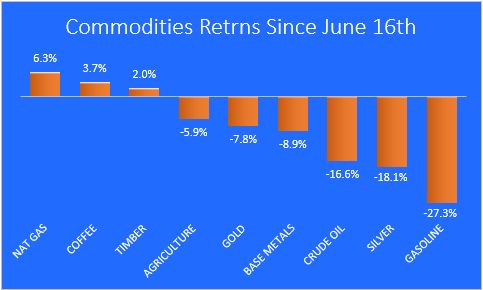

Commodities were the best performing asset class earlier in the year but they are undergoing a sharp correction now. Energy and agriculture stocks had been leading this asset class higher before the most recent correction started on August 17th.

The big winners in the asset class category are US stocks and US REITs.

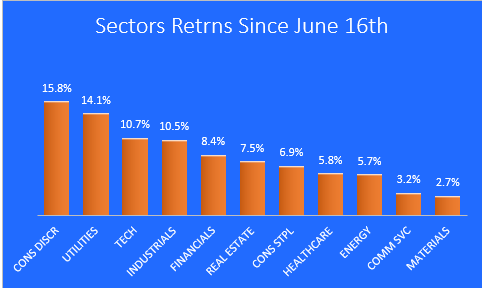

Stock Market Sectors

The big winners since June 16 are the beaten-down Consumer Discretionary and Technology stocks. Utilities have been outperforming all year.

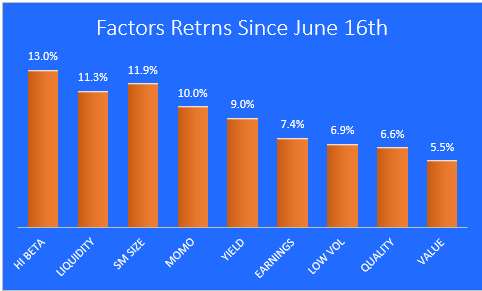

Stock Market Factors

The market X-ray shows that high beta stocks are the most preferred factors since June 16. Value stocks are struggling to keep up with growth stocks. And small stocks are enjoying a nice rebound.

Commodities

When we drill down into the commodities asset class we find three that are above water - Natural Gas, Coffee, and Timber. Gasoline, Oil, and Silver have corrected sharply.

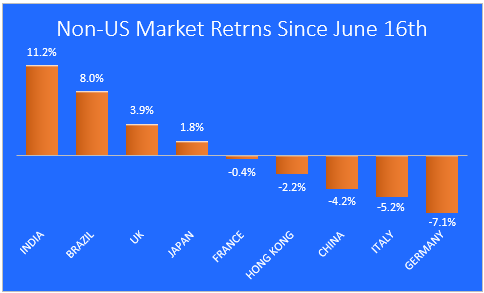

Foreign Markets

India and Brazil are leading the way higher in this group, while Germany and Italy are suffering due to their dependence on Russian energy imports.

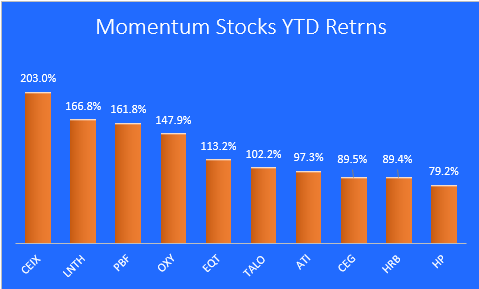

Momentum stocks

The chart differs from the others in that it shows the YTD gains for the highest momentum stocks in the S&P 1500 Composite Index.

Note that the chart is dominated by energy names, even though they have pulled back sharply since August 16th.

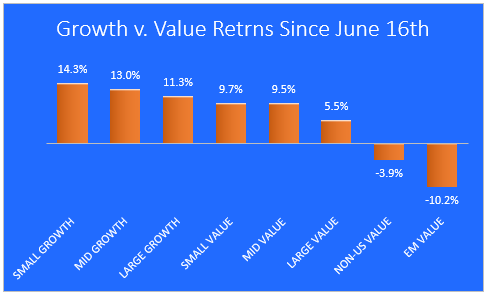

Stock Styles

The market X-ray shows that value stocks are lagging behind their growth counterparts during this downturn. I still think that value will continue to deliver throughout the rest of year.

Final thoughts

For the rest of 2022, I still like energy, commodities, healthcare and utilities. I lean towards value over growth. For non-US markets, European countries like Germany, France, and Italy will continue to struggle until they secure alternative sources of energy. The wild card is China, If China goes down, they could drag much of the developing world with them.

Investors mistakenly believed that the Fed was nearing the end of the rate hike process and they would pivot from tightening to loosening by early next year. However, the Fed has now made it clear that they are going to tighten more aggressively and for longer than what was being priced in. If we see a lower print on the CPI for August, I think we could see another rally attempt.

Added to inflation and recession worries is the persistent decline in earnings growth estimates. If estimates for this year and next year continue to come down, I think the market will react badly.

I'm hopeful that we will end the year somewhere around 4500, but we will undoubtedly do some backing and filling along the way. We may have already seen the bottom, but the dip-buyers must follow through when the next rally comes.

Monthly returns tell the story

A quick glance at the chart below tells the story. The rally-sellers dominated the action in January, February, April, June, and August. The dip-buyers tried to take back control in March, May, and July. They nearly succeeded in the two months from June 16 to August 16 by taking the market up 17.4%. It has all been downhill since then.

Global Market Indices

Today's market X-ray shows the returns for each index, asset class, sector, and so on, since the recent low point on June 16th. You can see what's leading the market and what's lagging behind. For reference, the S&P 500 is up 7.9% since June 16th..

Of the global indices, US small caps are in the lead, followed by the NASDAQ.

On a relative basis, U.S. stocks are trouncing non-US stocks and global bonds since June 16th.

All of the return data in this article is from Morningstar.

Global Asset Classes

Commodities were the best performing asset class earlier in the year but they are undergoing a sharp correction now. Energy and agriculture stocks had been leading this asset class higher before the most recent correction started on August 17th.

The big winners in the asset class category are US stocks and US REITs.

Stock Market Sectors

The big winners since June 16 are the beaten-down Consumer Discretionary and Technology stocks. Utilities have been outperforming all year.

Stock Market Factors

The market X-ray shows that high beta stocks are the most preferred factors since June 16. Value stocks are struggling to keep up with growth stocks. And small stocks are enjoying a nice rebound.

Commodities

When we drill down into the commodities asset class we find three that are above water - Natural Gas, Coffee, and Timber. Gasoline, Oil, and Silver have corrected sharply.

Foreign Markets

India and Brazil are leading the way higher in this group, while Germany and Italy are suffering due to their dependence on Russian energy imports.

Momentum stocks

The chart differs from the others in that it shows the YTD gains for the highest momentum stocks in the S&P 1500 Composite Index.

Note that the chart is dominated by energy names, even though they have pulled back sharply since August 16th.

Stock Styles

The market X-ray shows that value stocks are lagging behind their growth counterparts during this downturn. I still think that value will continue to deliver throughout the rest of year.

Final thoughts

For the rest of 2022, I still like energy, commodities, healthcare and utilities. I lean towards value over growth. For non-US markets, European countries like Germany, France, and Italy will continue to struggle until they secure alternative sources of energy. The wild card is China, If China goes down, they could drag much of the developing world with them.

Investors mistakenly believed that the Fed was nearing the end of the rate hike process and they would pivot from tightening to loosening by early next year. However, the Fed has now made it clear that they are going to tighten more aggressively and for longer than what was being priced in. If we see a lower print on the CPI for August, I think we could see another rally attempt.

Added to inflation and recession worries is the persistent decline in earnings growth estimates. If estimates for this year and next year continue to come down, I think the market will react badly.

I'm hopeful that we will end the year somewhere around 4500, but we will undoubtedly do some backing and filling along the way. We may have already seen the bottom, but the dip-buyers must follow through when the next rally comes.

Originally Posted on zeninvestor.org