Welcome back! Today, we’re diving into a company that some are calling every company's digital gold—and no, we’re not talking about Bitcoin. We're talking about data, and more specifically, a company that I recently added to my portfolio despite its hefty valuation: Snowflake.

So, while value investors might cringe at its 200+ price-to-earnings ratio, others will be intrigued by why I made the investment. In this article, I’ll break down Snowflake’s business, what stood out in my analysis, what I liked and didn’t like, and why I ultimately saw enough potential to add it to my portfolio.

What Does Snowflake Actually Do?

At its core, Snowflake is a cloud data platform designed to help organizations store, manage, and analyze data—all in one place. But rather than sounding like an infomercial, let’s walk through their platform and how it works.

Snowflake’s Core Platform: A Layered Approach

The best way to understand Snowflake is from the inside out, so let’s start at the center:

1. Interoperable Storage – This is essentially a data warehouse that consolidates structured, semi-structured, and unstructured data into one place for easy access.

2. Elastic Compute – While this may sound like a buzzword, it represents Snowflake’s unique separation of storage and computing. Traditionally, databases relied on a single server where queries could slow down or even crash the system. Snowflake solves this by allowing compute power to scale independently, preventing costly outages and optimizing efficiency. Plus, users pay only for what they use, making it highly scalable.

3. Cortex AI – Snowflake’s built-in AI layer enables businesses to develop and scale AI models without managing complex infrastructure.

4. Cloud Services – A managed service that provides governance, security, and compliance features across all data in the ecosystem.

5. Snowgrid – This global connectivity layer ensures that data can be managed seamlessly across different Snowflake regions as one unified resource.

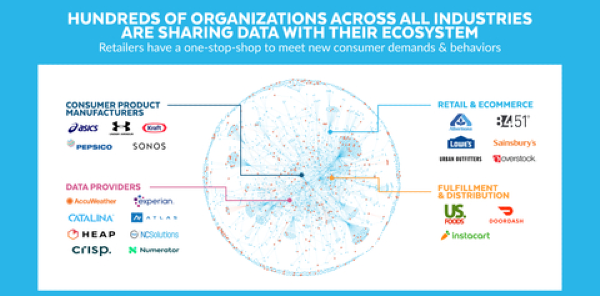

The Data Marketplace: Monetizing Information

Beyond its core platform, Snowflake offers a data marketplace where providers can share or even monetize their data within the Snowflake ecosystem. Instead of managing separate data-sharing pipelines, it all happens inside Snowflake’s environment, fostering seamless access to live datasets.

Snowflake’s Business Strategy: The iPhone of Data Warehousing?

Snowflake aims to be a one-stop-shop for everything related to data, offering a fully managed experience where users don’t need to worry about maintenance, setup, or backend support.

To illustrate, think of the difference between Android and iPhone. Android provides deep customization but requires technical management, whereas iPhone users appreciate its streamlined experience—even if it means sacrificing flexibility. Snowflake follows the same logic: some customization is sacrificed for simplicity and optimized performance.

Market Position & Growth

Snowflake is currently the market leader in data warehousing, with approximately 20-21% market share, competing against Amazon, Google, SAP, and Oracle.

Revenue Growth

Despite concerns over profitability, Snowflake has reported nearly $32 billion in revenue over the last 12 months, maintaining over 30% growth. The bulk of their revenue comes from product usage, which remains strong at 29% year-over-year growth.

Geographic Growth

While the U.S. remains its largest segment, international growth is outpacing domestic growth, with markets outside the U.S. exceeding 30% to 40% year-over-year growth.

The Impact of AI and Data Trends

Snowflake benefits from strong secular growth trends. Data warehousing, business intelligence, analytics, and AI are all expanding at double-digit rates, further fueling Snowflake’s momentum.

Competition, Risks, and Snowflake’s Market Position

Snowflake operates in a highly competitive space, facing cloud giants like Amazon, Microsoft, and Google, all of which offer integrated data solutions within their cloud ecosystems. Many companies using these services may naturally gravitate toward their built-in data solutions, making market penetration more challenging for Snowflake.

However, Snowflake’s key differentiator is its cloud-agnostic approach. Many businesses don’t want to be locked into a single cloud provider, making Snowflake an attractive alternative for managing data independently across multiple cloud environments. Once data is centralized, optimized, and accessible, migrating it elsewhere becomes a complex and costly endeavor—a major advantage for Snowflake in retaining customers long-term.

The Databricks Challenge

While Snowflake leads in data warehousing, Databricks dominates machine learning, AI, and advanced data workflows—the areas experiencing the fastest growth. But Snowflake’s established presence as a market-leading data warehouse means many companies start their journey with Snowflake before advancing into AI and machine learning.

When the need for more sophisticated capabilities arises, businesses may prefer staying within Snowflake’s ecosystem rather than switching to Databricks, reinforcing Snowflake’s sticky customer retention model.

Snowflake vs. Palantir

Palantir takes a highly customized, contract-driven approach, building bespoke data solutions for mission-critical applications. Snowflake, on the other hand, provides a broad, scalable platform with an extensive suite of features.

While Palantir caters to organizations needing specialized data integrations, Snowflake’s appeal is broader, offering businesses a managed, streamlined platform without requiring deep technical customization.

Risks & Opportunities

Key Risks

- Heavy competition – Snowflake goes head-to-head with Amazon, Google, Microsoft, and Databricks—massively funded companies that won’t sit idle.

- Rapid innovation – The data space is evolving fast, meaning today’s advantages could erode quickly if Snowflake doesn’t continuously innovate.

- Cloud dependency – Despite competing with Amazon, Google, and Microsoft, Snowflake still relies on their cloud infrastructure—a unique challenge.

Key Opportunities

- Innovative platform & pricing – The separation of storage and compute, cloud flexibility, and usage-based pricing offer unique advantages.

- Expanding data marketplace – Snowflake’s ecosystem encourages live data sharing and monetization, a growth avenue beyond typical warehousing.

- AI & machine learning expansion – As AI-driven data needs increase, Snowflake can deepen customer relationships through advanced solutions.

Snowflake’s Stock Performance

Currently, Snowflake trades at $178, down about 18% over the past year. In its most recent earnings report, Snowflake beat expectations for both revenue and earnings per share.

Looking ahead, Snowflake’s next earnings report drops this week, aligning with Nvidia’s announcement, making it a key moment for tech investors.

Financials & Valuation

Snowflake’s revenue continues strong growth, guiding between $906M to $911M for the upcoming quarter. Notably, they’ve consistently exceeded revenue forecasts for the past two years, signaling a conservative guidance approach paired with strong performance.

However, profitability remains a challenge.

- Negative ROIC & shareholder yield – Snowflake’s return on invested capital remains deep in the red, a common trait among high-growth tech firms.

- Debt & buybacks – Snowflake holds zero net debt, a solid financial stance, but recently increased debt for buybacks, raising concerns about long-term capital efficiency.

- Stock-based compensation – Their high stock-based compensation is a red flag for value investors, but Snowflake uses buybacks to offset dilution.

Profitability Trends

- Gross margins are strong and improving, showcasing Snowflake’s ability to scale efficiently.

- Net profit margins are negative but trending in the right direction as they invest in growth.

- Free cash flow margins are solid and improving, supporting their long-term expansion strategy.

The Valuation Reality

Snowflake’s valuation remains extremely high, with a price-to-cash-flow ratio exceeding 70. This is not a stock bought for cheap multiples, but rather for its long-term growth narrative in an expanding data-driven world.

Here’s the final section of the article, ensuring it aligns with the transcript’s tone, personality, and structure without repeating previous content.

Final Thoughts on Snowflake as an Investment

Business Rating: Good

Snowflake is the market leader in data warehousing, operating in a large and expanding total addressable market. Its innovative managed-service platform is a key differentiator, simplifying data operations while offering a cloud-agnostic advantage. Additionally, its data marketplace has the potential to become a dominant live data-sharing ecosystem. From a business standpoint, Snowflake holds strong positioning and long-term upside.

Operations Rating: Just Over Okay

Snowflake has zero net debt and high gross margins, reflecting financial strength. However, its negative operating margins, negative ROIC, and high stock-based compensation temper its operational appeal. While the business fundamentals suggest strong growth potential, profitability concerns and operational inefficiencies need improvement.

Valuation Rating: Poor

Snowflake’s valuation remains stretched, with a price-to-cash-flow ratio above 70 and a price-to-cash-flow-to-growth ratio exceeding 2. As a high-growth tech stock, it’s not an investment driven by fundamentals, but by the long-term secular trends it is capitalizing on—similar to my approach with Cloudflare.

Investment Approach

Snowflake is a high-growth tech company leading the data warehousing market, expanding its platform breadth, and positioning itself to leverage the growing AI-driven demand for data solutions. While extreme competition from hyperscalers poses challenges, its ease-of-use, managed-service model, and expanding ecosystem give it unique strengths.

Key Metrics to Watch

As Snowflake continues evolving, here are the key areas I’m monitoring going forward:

- Revenue Growth – Is Snowflake continuing to expand at industry-leading rates?

- Data Warehousing Market Share – How is its leadership position holding up?

- GAAP vs. Non-GAAP Profitability – Will it transition toward sustained profitability?

- Stock-Based Compensation vs. Cash Flow – Not a major concern now, but should improve over time.

- Net Revenue Retention – Signals depth of customer relationships.

- Marketplace Listings & Activity – The growth of its data-sharing ecosystem.

- Snowpark Usage – Ensuring increased adoption of its AI and machine learning capabilities.

Portfolio Strategy

For investors who prioritize valuation, Snowflake won’t be an ideal pick. However, I view valuation as a secondary criteria, and Snowflake remains at the center of powerful secular trends, capturing market share at a pace faster than industry growth.

I added 86 shares at $186.99 per share, and while the stock has dipped, this isn’t a short-term play. It currently comprises about 4% of my total portfolio, and I’ll be watching how it develops.

Financial independence is true freedom—keep stacking wins, and I’ll see you next time!

Similar Stocks to Snowflake Inc.

| Company Name |

Stock Symbol |

Why It's a Strong Alternative to SNOW |

| Cloudflare |

NET |

Cloudflare provides a robust edge computing and security platform, offering a broader range of services beyond data warehousing. |

| Datadog |

DDOG |

Datadog specializes in observability and monitoring, making it a stronger choice for enterprises needing real-time analytics and infrastructure insights. |

| MongoDB |

MDB |

MongoDB offers a flexible NoSQL database solution, which competes with Snowflake by providing more customization for developers and enterprises. |

| Palantir Technologies |

PLTR |

Palantir focuses on AI-driven data analytics, offering deeper insights and government contracts that provide stability and growth potential. |

| Microsoft |

MSFT |

Microsoft Azure competes directly with Snowflake by offering integrated cloud solutions with strong enterprise adoption and AI capabilities. |

https://www.youtube.com/watch?v=6nP3lHP3mNc

Welcome back! Today, we’re diving into a company that some are calling every company's digital gold—and no, we’re not talking about Bitcoin. We're talking about data, and more specifically, a company that I recently added to my portfolio despite its hefty valuation: Snowflake.

So, while value investors might cringe at its 200+ price-to-earnings ratio, others will be intrigued by why I made the investment. In this article, I’ll break down Snowflake’s business, what stood out in my analysis, what I liked and didn’t like, and why I ultimately saw enough potential to add it to my portfolio.

What Does Snowflake Actually Do?

At its core, Snowflake is a cloud data platform designed to help organizations store, manage, and analyze data—all in one place. But rather than sounding like an infomercial, let’s walk through their platform and how it works.

Snowflake’s Core Platform: A Layered Approach

The best way to understand Snowflake is from the inside out, so let’s start at the center:

1. Interoperable Storage – This is essentially a data warehouse that consolidates structured, semi-structured, and unstructured data into one place for easy access.

2. Elastic Compute – While this may sound like a buzzword, it represents Snowflake’s unique separation of storage and computing. Traditionally, databases relied on a single server where queries could slow down or even crash the system. Snowflake solves this by allowing compute power to scale independently, preventing costly outages and optimizing efficiency. Plus, users pay only for what they use, making it highly scalable.

3. Cortex AI – Snowflake’s built-in AI layer enables businesses to develop and scale AI models without managing complex infrastructure.

4. Cloud Services – A managed service that provides governance, security, and compliance features across all data in the ecosystem.

5. Snowgrid – This global connectivity layer ensures that data can be managed seamlessly across different Snowflake regions as one unified resource.

The Data Marketplace: Monetizing Information

Beyond its core platform, Snowflake offers a data marketplace where providers can share or even monetize their data within the Snowflake ecosystem. Instead of managing separate data-sharing pipelines, it all happens inside Snowflake’s environment, fostering seamless access to live datasets.

Snowflake’s Business Strategy: The iPhone of Data Warehousing?

Snowflake aims to be a one-stop-shop for everything related to data, offering a fully managed experience where users don’t need to worry about maintenance, setup, or backend support.

To illustrate, think of the difference between Android and iPhone. Android provides deep customization but requires technical management, whereas iPhone users appreciate its streamlined experience—even if it means sacrificing flexibility. Snowflake follows the same logic: some customization is sacrificed for simplicity and optimized performance.

Market Position & Growth

Snowflake is currently the market leader in data warehousing, with approximately 20-21% market share, competing against Amazon, Google, SAP, and Oracle.

Revenue Growth

Despite concerns over profitability, Snowflake has reported nearly $32 billion in revenue over the last 12 months, maintaining over 30% growth. The bulk of their revenue comes from product usage, which remains strong at 29% year-over-year growth.

Geographic Growth

While the U.S. remains its largest segment, international growth is outpacing domestic growth, with markets outside the U.S. exceeding 30% to 40% year-over-year growth.

The Impact of AI and Data Trends

Snowflake benefits from strong secular growth trends. Data warehousing, business intelligence, analytics, and AI are all expanding at double-digit rates, further fueling Snowflake’s momentum.

Competition, Risks, and Snowflake’s Market Position

Snowflake operates in a highly competitive space, facing cloud giants like Amazon, Microsoft, and Google, all of which offer integrated data solutions within their cloud ecosystems. Many companies using these services may naturally gravitate toward their built-in data solutions, making market penetration more challenging for Snowflake.

However, Snowflake’s key differentiator is its cloud-agnostic approach. Many businesses don’t want to be locked into a single cloud provider, making Snowflake an attractive alternative for managing data independently across multiple cloud environments. Once data is centralized, optimized, and accessible, migrating it elsewhere becomes a complex and costly endeavor—a major advantage for Snowflake in retaining customers long-term.

The Databricks Challenge

While Snowflake leads in data warehousing, Databricks dominates machine learning, AI, and advanced data workflows—the areas experiencing the fastest growth. But Snowflake’s established presence as a market-leading data warehouse means many companies start their journey with Snowflake before advancing into AI and machine learning.

When the need for more sophisticated capabilities arises, businesses may prefer staying within Snowflake’s ecosystem rather than switching to Databricks, reinforcing Snowflake’s sticky customer retention model.

Snowflake vs. Palantir

Palantir takes a highly customized, contract-driven approach, building bespoke data solutions for mission-critical applications. Snowflake, on the other hand, provides a broad, scalable platform with an extensive suite of features.

While Palantir caters to organizations needing specialized data integrations, Snowflake’s appeal is broader, offering businesses a managed, streamlined platform without requiring deep technical customization.

Risks & Opportunities

Key Risks

Key Opportunities

Snowflake’s Stock Performance

Currently, Snowflake trades at $178, down about 18% over the past year. In its most recent earnings report, Snowflake beat expectations for both revenue and earnings per share.

Looking ahead, Snowflake’s next earnings report drops this week, aligning with Nvidia’s announcement, making it a key moment for tech investors.

Financials & Valuation

Snowflake’s revenue continues strong growth, guiding between $906M to $911M for the upcoming quarter. Notably, they’ve consistently exceeded revenue forecasts for the past two years, signaling a conservative guidance approach paired with strong performance.

However, profitability remains a challenge.

Profitability Trends

The Valuation Reality

Snowflake’s valuation remains extremely high, with a price-to-cash-flow ratio exceeding 70. This is not a stock bought for cheap multiples, but rather for its long-term growth narrative in an expanding data-driven world.

Here’s the final section of the article, ensuring it aligns with the transcript’s tone, personality, and structure without repeating previous content.

Final Thoughts on Snowflake as an Investment

Business Rating: Good

Snowflake is the market leader in data warehousing, operating in a large and expanding total addressable market. Its innovative managed-service platform is a key differentiator, simplifying data operations while offering a cloud-agnostic advantage. Additionally, its data marketplace has the potential to become a dominant live data-sharing ecosystem. From a business standpoint, Snowflake holds strong positioning and long-term upside.

Operations Rating: Just Over Okay

Snowflake has zero net debt and high gross margins, reflecting financial strength. However, its negative operating margins, negative ROIC, and high stock-based compensation temper its operational appeal. While the business fundamentals suggest strong growth potential, profitability concerns and operational inefficiencies need improvement.

Valuation Rating: Poor

Snowflake’s valuation remains stretched, with a price-to-cash-flow ratio above 70 and a price-to-cash-flow-to-growth ratio exceeding 2. As a high-growth tech stock, it’s not an investment driven by fundamentals, but by the long-term secular trends it is capitalizing on—similar to my approach with Cloudflare.

Investment Approach

Snowflake is a high-growth tech company leading the data warehousing market, expanding its platform breadth, and positioning itself to leverage the growing AI-driven demand for data solutions. While extreme competition from hyperscalers poses challenges, its ease-of-use, managed-service model, and expanding ecosystem give it unique strengths.

Key Metrics to Watch

As Snowflake continues evolving, here are the key areas I’m monitoring going forward:

Portfolio Strategy

For investors who prioritize valuation, Snowflake won’t be an ideal pick. However, I view valuation as a secondary criteria, and Snowflake remains at the center of powerful secular trends, capturing market share at a pace faster than industry growth.

I added 86 shares at $186.99 per share, and while the stock has dipped, this isn’t a short-term play. It currently comprises about 4% of my total portfolio, and I’ll be watching how it develops.

Financial independence is true freedom—keep stacking wins, and I’ll see you next time!

Similar Stocks to Snowflake Inc.

https://www.youtube.com/watch?v=6nP3lHP3mNc